Wills and Estates Planning

Death is unfortunately and sadly a part of life, but the time after death, for your family, friends and loved ones, can be significantly impacted depending on whether or not you have a complete and effective estate planning in place. Our Wills and estates lawyers at Solomon Hollett Lawyers can help you through this process by offering support, assistance and legal advice to give you peace of mind.

Having a Will and proper estate planning is imperative to ensure that your estate is fairly shared with your loved ones, and that your assets are protected and distributed to the right people. At Solomon Hollett Lawyers, we truly believe that having a suitable Will and estate plan is the most important gift you’ll ever give to those around you.

Our Wills and estates lawyers in Perth understand that each situation is different and getting to know the circumstances is essential to be able to give the right advice. Our experienced team will guide you through the whole process to ensure that you can make informed decisions during your Will and estate planning and be reassured that when the time comes, you have done everything you can to set up a smooth transition of inheritance to your loved ones.

Estate planning

Our Will solicitors at Solomon Hollett Lawyers can help with comprehensive legal advice and guidance when it comes to estate planning, ensuring that your family are provided for and well protected when the time comes. The experience and expertise we have in this particular field of the law has found us featuring on the prestigious peer-voted Doyle’s Guide annual rankings three years in a row.

Enduring power of attorney

An enduring power of attorney is a legal document that allows you to give authority to someone else to make decisions for you in financial and legal matters. An enduring power of attorney is ‘enduring’, in that it continues in full force and effect, even after you have lost testamentary capacity and can no longer make decisions for yourself. This is powerful document which can be dangerous if in the hands of the wrong person or if the document is drafted inaccurately.

Whether you are looking to have an enduring power of attorney put in place, need help understanding the rights and responsibilities that comes with a being appointed as an attorney, or even suspect that someone is abusing their power, talk to our team of Wills and estates lawyers. Sound legal advice and support from the right people is essential when considering a power of attorney.

Testamentary trusts

A testamentary trust is a trust that is created by a Will. Establishing a testamentary trust is an alternative to giving someone a share of your estate in your Will outright. There are a number of reasons why it might be a good idea for your assets to be left to someone on trust rather than put straight into their hands. For example, they might be a spendthrift and irresponsible with money, or there might be impending or possible threats against their own estate, such as a bankruptcy or Family Court proceedings. A testamentary trust can help to quarantine and protect assets, to ensure that your estate doesn’t go to unintended parties. They can also be a useful tool to minimise tax where the trust earns income.

Our Wills and estates lawyers at Solomon Hollett Lawyers have experience in drafting testamentary trusts for a variety of situations and can tailor a trust to suit the needs of your intended beneficiaries.

Reach out to our team today for a free 15-minute consultation where we can assess your situation and give you the right legal advice to move forward.

Frequently

asked

questions

Can’t find what you are looking for?

Why do I need a Will?

Wills are vital not just for saying who should benefit from your estate; they are vital for determining who should not benefit and why.

One of the great myths we hear time and time again is this: “I don’t need a Will, I’m married and so everything goes to my spouse automatically.” This myth persists even though it is just not true. We know why many people think this – in generations past, married couples often held all their assets jointly which meant it all went to the survivor, but these days with Super and life insurance and mortgages larger than ever, these things just don’t work.

A well-considered Will and estate plan can also protect loved ones from situations where a spouse ends up almost fighting their beloved young children and the trustee that acts for them for control of the estate, often held in a mandatory trust for the children until the children come of age. We’ve seen the most terrible situations here where the surviving spouse is unable to pay the mortgage or is forced to sell the family home as they simply cannot get control of the estate automatically held in their young children’s names.

If you have children under 16, then it is the way to appoint legal guardians. Choosing the right legal guardian for infant children is a decision that if wrong can outweigh everything else. We have seen sharks circling around infant children to try and get control of their trusts, or be legal guardians for all the wrong (financial) reasons.

You can use your Will and estate plan to make smart tax planning decisions to potentially save your beneficiaries significant sums that otherwise could be sucked out of your estate.

Ultimately, you can have your say, instead of leaving it to the winds of fate. And in doing that, you can leave a neat and decisive plan that works for all concerned, mastering the image and memory you leave behind.

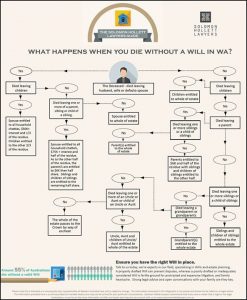

What happens if I don't have a Will?

Recent statistics tell us that over 40% of Australians die without a Will. That remarkable and troubling statistic has held pretty firm for years, so it is apparent that it is not for lack of education that people die intestate. But whatever the reason someone chooses not to write a Will, the consequences, although not the precise path by which they will apply, are pretty predictable.

For a start, the costs of applying to the Court for Letters of Administration (where there is no Will), instead of Probate (where there is a Will) are, at the very minimum, two or three times as much as the cost of a getting a good Will in place. Where there are complexities (and we shall get to those in a minute), the costs can and usually do skyrocket. But increased legal costs are just the start of the agony that usually accompanies intestacy.

If you don’t have a Will and own more than $10,000 worth of any sorts of assets, as an intestate your estate is carved up according to the strict mandated intestacy formula that says who gets what, and this is key – you have no say in it, and the administrator of your estate cannot alter the formula either – its set in stone. The graphic here gives a good indication of the strict formula set out in the Administration Act WA (1903), dictating who your beneficiaries will be, and what share they will receive. As you can see, without a valid Will, the operation of these automatic intestacy provisions can lead to some pretty disastrous or inequitable outcomes. The Administration Act also gives the person with the greatest share of your estate the first opportunity to be the Administrator of your Estate (the equivalent of the Executor when there is a Will). Again, without a valid Will, you have no say in this at all.

The other thing to remember is that the intestacy provisions have not been updated in some 30 years – so amounts in the formula (for example $50,000 to a spouse) are based on the WA cost of living two generations ago. When the legislation was last amended, $50,000 could buy a modest house here in Perth which of course is so far from the case now. That being said, there are changes afoot – the WA Parliament is currently considering proposed amendments to the Administration Act to increase the partner’s legacy to $435,000, so watch this space!

In any event, before you question the results of intestacy created by Parliamentarians, remember that it is a legislative back up plan. You are supposed to have a Will, and as a responsible adult who owns assets of even modest value you are expected to have a Will, and the formula is really to try and create a sort of average for those that die without a Will. It is hardly ever going to match your own situation, because that is what your Will is supposed to do. Remember this when contemplating your own estate planning situation – the default position is that you do have a valid Will. The back-up plan of the Administration Act intestacy provisions is no more than a back-up plan, and not a particularly good one at that. If you don’t have a Will then the law assumes you thought the legislative back-up plan was good enough, and so that is what your loved ones are left with.

1 – Having the last word: Will making and contestation in Australia, Op. cit. p.2

What are the common myths or misconceptions you see all the time when it comes to dying without a Will?

Another myth we hear often is that because my Will is going to be challenged there is no point in having one in the first place. This is like saying any castle I live in is going to be attacked so I might as well live in a tent.

A myth that still circulates is that the executor of your Will can do as they please with the estate assets, including making up their own mind on who gets what, which is far from the truth. In rare circumstances some Wills are specifically drafted to give their executor very broad discretionary powers, but unless you create such a Will, your executor is bound to follow your Will to the letter.

Having the right Will in place gives you the right and best protection, and gives you the peace of mind that those closest to you will be looked after in the right way, given the powers they need to benefit the most, and has the best shot at preserving the wealth you’ve worked so hard your whole life to achieve. Needless to say, it also takes away so much of the emotional cost of not having your affairs in order.

When or how often do I need to update my Will?

For this reason, we recommend reviewing your estate plan every two to three years – this does not mean it needs to be re-done, by any means, it may simply involve reading over the documents you have in place and satisfying yourself that they still reflect your wishes.

However, there are certain life events that should also trigger a review of your estate plan, and they include the following:

Changes to your relationships or those of your children or grandchildren – this includes

marriage, separation, divorce, and new partnerships. It is especially important to remember that your Will is automatically revoked when you marry or divorce – but be careful to remember that entering a new de facto relationship or ending one does not revoke your Will.

Changes to your superannuation.

Significant changes to your asset pool, such as acquiring property, investments, business interests, investment properties, family trusts or the like.

Births and deaths of family members and other potential beneficiaries.

Significant travel.

Disability, illness, bankruptcy, medical conditions or addiction – for you or your potential beneficiaries.

If you come into money, such as inheritance, and need to protect it or future proof it against possible relationship breakdowns, or business or financial risk or to ensure it is quarantined for your own bloodline.

Why is it so important to keep my Will up to date?

It’s a very different landscape than it was even just 5-10 years ago, and it’s more important than ever to keep up to date to ensure you have the right protection in place.

Why such rapid change? Australian family structures, business structures and asset pools are all becoming more complex, with precedents and laws changing to keep up with changes in society. 2017 also saw a raft of changes around superannuation laws with some flow on effects when it comes to estate planning and some interesting cases around binding financial agreements that highlight the importance of the right advice. We of course also saw the landmark decision to legalise same sex marriage and with every marriage (and divorce) automatically revoking a Will the flow on effects are becoming evident.

In Western Australia we’re also seeing a marked rise in the number of people challenging or contesting an estate. We put this down to a number of factors, including the rising value in property asset pools and the rise in value of life insurance and superannuation. As asset pools continue to grow, so does the risk of a challenge as the size of the prize increases. We’ve also seen a host of very high-profile cases with well-known families contesting estates hit the front pages here in Perth – increasing awareness on the ability to challenge.

The number of intestacy cases (someone dying without a valid Will in place) is still alarmingly high here in Perth – yet another factor behind the rising numbers of estates being challenged. With intestacy so often proving both an emotional and financial nightmare to unravel the automatic beneficiary provisions set down by old and increasingly outdated laws, it’s not hard to see why so many of these are ripe for legal challenge.

Recent statistics suggest around 59% of Australians have a Will in place. Our job is to ensure the number continues to rise; to see more West Australians with the right Wills and estate planning in place – Wills that are well drafted and well considered and that make proper provision for loved ones. It’s all about leaving the right legacy in place.

What happens to assets acquired after a Will is written?

But essentially the answer to this question really depends on what your Will actually says.

For example, if a person has total assets of $310,000 and they write a Will which says “ I leave $100,000 to each of my three children and the remainder to my favourite charity ” then that Will covers all those assets at the time the Will was written fairly neatly. If the person dies 20 years later and those assets are now $1m, then the children still get only $100,000 each and the charity gets $700,000 – almost certainly not what was intended.

Again, the answer to this question depends on what your Will says and how well its written to accommodate changes in your assets. We would routinely address this by writing a Will which says “I leave 97% of my estate to my three children equally, and 3% to my favourite charity.” With this type of focus, even if you acquired millions of dollars the outcome is always the same.

It is also important to remember that different sorts of assets have different paths they follow – jointly held assets go to the survivor, for instance and super goes according to the terms of the Super fund you are a member of, and family trust assets don’t go anywhere and stay in the trust.

How much will my Will cost?

However, here is a general range for the most common documents we draft, based on a simple landscape:

| Service | Approximate fee |

| Simple Will | $1,000 – $1,700 |

| Will incorporating testamentary trust | $1,700 – $3,000 |

| Enduring Power of Attorney | $350 – $600 |

| Enduring Power of Guardianship | $350 – $600 |

| Advance Health Directive | $450 – $900 |

| Binding Death Benefit Nomination for Self-Managed Super Fund | $900 – $1,500 |

| Irrevocable resolution of company or trust | $900 – $2,000 |

| Deed of Variation of Trust | $900 – $2,500 |

| Establishment of Discretionary Trust | $1,500 – $2,500 |

| Establishment of Discretionary Trust and establishment of corporate trustee | $2,000 – $3,000 |

All prices are exclusive of GST and disbursements (such as Landgate and ASIC searches and Landgate registration fees for Powers of Attorney). Complex estate planning, for example the creation of multiple testamentary or protective trusts, or special disability trusts for special needs beneficiaries within a Will increase the complexity and naturally increase the costs.

However, there is often a good economy of scale in creating multiple documents at the same time for a client, and the total fees for a suite of documents will usually be less than the component prices of each single document.

For example, a Will for one person including a Testamentary Trust might be $2,500 plus GST, but if it is for both a husband and wife and they are essentially mirroring each other, the combined cost for two is not $5,000 plus GST may be as low as $3,000 plus GST. Naturally this is only indicative, because everyone is different and looking to achieve different outcomes.

You will be able to find law firms who provide the above services more cheaply. You will also find firms that charge far more. Some firms’ services don’t extend to the full range of the above work. It will also come down to the experience and quality of the lawyer drafting it for you and here the old adage often applies in that you get what you pay for.

Once we know a little more about you, we will be in a much better position to evaluate your needs and give you a firm quote. If you’d like to know more about what our firm can offer, simply give us a call or take advantage of our free 15 minute consultation by providing your details here on the site via one of our forms. Once we know a little more about you and evaluate what you need to best match your situation, we will provide you with a firm quote.

How do I look after a beneficiary with a disability in my Will?

If you have a child or other loved one with a disability, they may need special protection after you’ve passed on.

For example, if they are unable to work, they may need more resources than your other children- what is proper and adequate for a disabled child who cannot earn an income is likely very different indeed from that you would leave a child who is earning a very good wage as a carpenter, so how you decided to split your estate between them is a key decision.

Additionally, the share you do leave a child with a disability may need its own form of protection within your Will, in a testamentary trust, to prevent it being squandered or spent unwisely, or if the disabled child is at risk of being victim of scams or predatory behaviour.

Children with severe disabilities can also benefit from the use of what is known as a special disability trust, that allows you to leave them large sums of money that will not affect their pension or disability payments they receive from the government.

There are many types of trusts – and you can customise them very greatly to make specific sorts of provisions, but care needs to be taken in drafting these to ensure they maximise the outcome for the beneficiary.

Can I ask a beneficiary to take a DNA test?

This is a very tricky, and contentious area. If you suspect that a child or a parent may not be your natural relative, you should talk to us first about strategies going forward – sometimes once the cat is out of the bag it can trigger a raft of follow on issues that can balloon into major complexities and can destroy families and relationships. Needless to say – we’ve worked with many families in this situation and we’re more than happy to share our experience on how best to navigate.

Where should I keep my Will?

There is no register of Wills, no formal list you can go and search to see if someone has one. But wherever you keep your Will, it’s always a good idea to make sure your executor knows where to find it. You don’t need to give anybody access to your Will during your lifetime, or even to show them what it says – and that includes your executor – but they should know you have one, and where to look for it when the time comes.

Can my Western Australian Will govern assets held in another State or country?

In short, the ability of your Will to govern assets held in another State or country will depend on three questions:

What kind of asset it is

Where the deceased live at their date of death

Where the asset is located

An asset is categorised as moveable or immoveable, meaning it can either be transported from place to place (like cash, furniture, and personal effects), or it cannot (like land). If it is a moveable asset, then the law of domicile (where the deceased usually lived) applies. If it is an immoveable asset, the law of the land (where the asset is located) applies.

Here’s an example: Paul was born in Europe but immigrated to Melbourne with his family when he was 25 years old. Five years ago, he moved to Perth, but his parents stayed in Victoria. He has a WA Will. He has a home in Perth, but he also owns some land in Europe and left some personal items in his parents’ care. When Paul dies, his estate consists of moveable property in Melbourne and immoveable property in Perth and in Europe. Paul lives in WA, and so his WA will can cover his moveable property in Melbourne as well as his immoveable property in Perth. It cannot, however, dictate what happens to his land say in Germany. This land is governed by German law.

There is also something called an ‘International Will’ which comes about via an agreement and international treaty between countries around the world. These are unfortunately not the solution they sought to be when they were first floated in the 1970’s. Many countries have not signed up to the treaty, and for those that have, the International Will still is complex and cannot accommodate any of the unique aspects that each country might have around trusts and tax law for example.

There is a lot more to it than this, but just from the brief example above you can see that these matters can quickly become very complicated. Particularly where immoveable property is involved, unless the person drafting the Will has a thorough knowledge of the law of the overseas or even interstate jurisdiction, it is a good idea to engage a legal practitioner local to that jurisdiction to prepare the Will. This is not necessarily the case for moveable property however, which can frequently be dealt with in your WA Will, and so your first port of call where you have assets in multiple jurisdictions should be a WA expert who can give you reliable advice about what your next steps should be.

What are the worst mistakes you see when it comes to people’s Wills I should avoid?

As experienced estate planning lawyers, we see, with quite alarming regularity, the same mistakes made over and over again.

Some of them are understandable, but some have their genesis in nothing more than myth, superstition and urban legend. All of them are usually disastrous. Here are our top six:

- Believing you don’t need a Will because you’re married. This one is disarmingly common. We see many people who are genuinely shocked to hear that if they died without a Will, their darling spouse would get only one third of their assets, and their children the rest. The common misconception is that a spouse automatically gets the lot. We think this myth has penetrated so deeply into society because previous generations owned simple assets and held them equally simply with a spouse. But this myth is shattered in our modern society where assets and family landscapes of dependent children and grandchildren, stepchildren and de facto spouses and former spouses are commonplace. The actual consequences of dying intestate (without a Will) are many and complex and stretch well beyond the above scenario.

- Giving someone a nominal amount in your Will defeats their ability to challenge your will. It doesn’t. What matters is whether the amount you have left them is adequate and proper in all the circumstances, which is a very subjective test with many considerations that vary from person to person and change from time to time.

- Believing that you don’t need a Will because you have no assets. Very commonly held belief mainly of young adults, new into the workforce and with little savings. So often the young forget about their Super and life insurance. You may have only just started your first real job and have a few bucks in Superannuation accumulated, but there is a better than fair chance you also have a life insurance policy attached to that super fund you may not have even realised you opted into by ticking a box on the Super forms. $250,000 in life insurance is very common, but it can be much more. Also, if you die unexpectedly because of injuries sustained at work or in an accident then you can probably add a whole lot more into your estate.

- Not understanding estate versus non estate assets. The very common error here is thinking you own something when you don’t, and also not dealing properly with those assets. Classically, these are trust assets, either things in a family trust or superannuation. Whilst to the world at large it appears you own those assets, you don’t, and they have to be dealt with by other means, such as making binding death benefit nominations for your super or changing control of the family trust. A Will simply does not touch them, unless specific and very deliberate action is taken to channel those assets into a Will. Likewise, many of us own our homes and other assets jointly and depending on what sort of joint ownership determines if your half is in or outside the Will.

- Including a clause in your Will that if anyone challenges, they get nothing. If only this worked! it has no weight at all unfortunately. The rationale is that the right to challenge a Will is given to a person by Parliament (via the Family Provision Act 1972) and you cannot take that right away.

- That a $50 DIY Will from the newsagent or a generic online template is perfectly fine. As Master Sanderson of the WA Supreme Court has repeatedly said, that is “the curse of the homemade Will”. They are more often than not ambiguous and inadequate. The legal costs of fixing them up and dealing with the fallout after death are usually orders of magnitude more than the costs of having a good lawyer written Will done in the first place – it is one of the greatest false economies of all time – not only the monetary costs that have to come from the estate (so reducing the amount for the beneficiaries) but the human costs of stress, long drawn out processes and disputes and often Court battles.

Can I specify in my Will if I’d like someone NOT to receive anything and can this be upheld?

You can leave your worldly wealth to anyone you like. You can leave it all to a performance artist to heap into a pile and burn it, if you so desire.

But surrounding this freedom is a moral obligation to make sure family and those in need or dependent on you are looked after. So if you have a child for instance who is dependent on you and you leave them nothing, they are very likely to challenge and be successful. However, if you write in your Will that you want nothing to go to your brother, then because they are not able to challenge your Will (see above FAQ ‘Who Can Challenge My Will’) then that provision will be upheld.

Can I use a DIY online or newsagent-type Will template?

Yes you can. You can also decide to service your own car, or build your own house. But if you don’t have the skills and knowledge, your car won’t run and your house will fall down around your ears.

Recent statistics tell us that about 40% of all Australians die without a Will.[1] But at some point, all of us have at least started to consider what a Will is and how to go about getting one done.

And in that thought process most of us have considered, at least for a minute or two, scouring online for a good-looking template, or going down to the newsagent and buying a Will Kit for $40 and doing it yourself. ‘How hard can it be?’ we ask.

The reality is that so many of these homemade Wills end up in Court. The money saved by not getting it done by a lawyer and doing it yourself is mere pocket change compared to the costs of the dispute that quickly eat into the size of the estate.

Sadly too, we have seen precious few of these homemade Wills that actually properly reflect what the Will maker (the testator) actually thought they were achieving.

Ambiguous language, quasi legalistic terms that have doubtful (or worse) meaning, phrases such as ‘next of kin’ or ‘issue’ which mean different things to different people, trying to gift away assets you don’t actually own (the main example being the family home owned as joint tenants with someone else) trying to leave superannuation and life insurance in your Will (reader beware, this is the most common fatal error in Will drafting) and trying to write people out of Wills who ought not be entitled, are just some of the things that go wrong.

If you are in a second marriage or de facto relationship or you and your spouse have children from a former relationship, basically all bets are off – your Will is complex, immediately – just by virtue of how your family is made up. Do not attempt to write your own Will.

To everyone else, it is possible, but risky.

Occasionally one of these homemade Wills actually passes the first test and is able to be admitted to probate. All too often however there are spelling errors or different coloured pens used to sign by different witnesses, amendments and crossings out, sometimes staple marks, changes of date and names, occasionally coffee or red wine stains. Each of these things makes the homemade Will that much harder to get admitted to probate, which invariably means higher legal costs.

But even if there are no drafting errors, the real costs come where disenfranchised family members dispute the Will because it was drafted poorly – accurately, perhaps, but without proper consideration of the law.

These costs are much more than mere money, which can run in the hundreds of thousands of dollars depending on the capacity or appetite of the family to fight. The toll often includes the emotional costs of ruined relationships, families torn apart and disharmony that can never be healed.

Sadly, we see second and third generations of the same family disputing every Will that comes up in an attempt to redress the first badly drafted or careless Will that caused the upset, decades ago. This is something that could have been completely avoided or enormously reduced at least, if only the Will drafter had taken some sound legal advice in the first place.

We can understand the rationale behind wanting to draft your own Will. Firstly, it is a private document and so to divulge your true situation to a lawyer requires great trust and confidence in the lawyer. Secondly, the sense that ‘why pay for something I can do myself’ attitude is prevalent, and it’s dangerous.

Successful and smart estate planning, likewise, needs an expert on side. Unless you are an estate planning lawyer, the subtleties and complexities that are just below the surface that make up the everyday landscape of Wills and estates are something of a mystery. Small changes to Wills can make enormous changes to the result; a good Will is an object of crafted perfection and high precision, which has covered as many of the ‘what if’s’ as possible, and yet is readable and understandable.

This of course does not even take into consideration any of the enormous benefits that you can access in your estate planning by considering things such as testamentary trusts, protective trusts and special provisions to prevent bankrupt beneficiaries or divorcing children losing their inheritance.

Well considered estate planning is the key. Estate planning includes Wills, usually as the starting point (but rarely do it yourself Wills) but includes not only a raft of other legal instruments but includes a holistic approach to working out your affairs and what happens to your assets and who will look after your loved ones when you die.

An estate plan involves a root and branch analysis of your assets, your family commitments, your risks and how to accommodate them all into a plan where what you have can be left to those you leave behind in the right manner, the right amounts and at the right time.

We start with an analysis of your assets, and dividing them into what are called ‘estate’ and ‘non estate assets. They must all be treated carefully.

For example, you might think you own your home, and maybe you do if you don’t have a mortgage over it (which if you do also should be factored into how you deal with that when working out how to deal with the family home).

But many times we see, especially in married couples, that the home is owned as joint tenants. That means the survivor of two automatically gets the home, no questions asked. It does not fall into the Will, until the second of the two dies. This is especially a tricky issue for those on their second marriage or with step-children and children from other relationships.

In these circumstances, you may need to leave your half of the family home first to your new spouse, for them to live in for the rest of their days, and when they have finished with it, only then do your own kids get your half. A ‘Life Interest’ this is often called, but in reality is a form of testamentary trust established in a Will. But if the house is held in joint tenancy then this cannot happen.

In this case, it is not unusual for us to advise clients to change the tenancy of the house, from joint tenants to tenants in common, and when that is done, then half the house can be left in a Will or a life interest created.

Superannuation and life insurance, which we pretty much all have, must be looked at carefully.

Suffice to say, super is not in your Will. It is a trust asset, and can be controlled, but only by taking very particular steps that vary according to what super fund you are a member of, and what family members you leave behind and how dependent they are on you.

Life insurance itself is a common thing to look at, and more specifically, whether you need more life insurance to ensure you leave something other than debts to your dependents. We often refer our clients to financial planners who can arrange better life insurance to make sure spouses and children are properly looked after on death.

There are also touchy and delicate subjects to address in making Wills. It is not uncommon for a person to have a child who has special needs, a disability or high-risk factors such as a gambling or drug problem. More often than not we’re dealing with families with complex rifts between their children and again this is something that has to be considered and accommodated. These beneficiaries cannot just be written out of Wills: careful consideration to each one and their needs must be given, or else the risk of a challenge to the Will, upsetting everything, is likely.

With a good estate planning lawyer by your side, your Will can accomplish miracles; provision for a special needs beneficiary can be made in a way which does not affect their disability pension, or a testamentary trust to protect a spendthrift beneficiary so that they do not burn through their whole inheritance in a heartbeat. Testamentary trusts can also approach the idea of a beneficiary getting divorced, and special provisions can be included to protect an inheritance from so called ‘gold diggers’.

So ultimately, yes, you can make a Will kit or online template type Will. You can also go for the cheap and cheery mobile Wills type legal outfit where a business charges you only a few hundred dollars and can only afford an hour or so to change names on a templated document. We would caution against any of these options. The prospects of your Will actually working as you thought it can be low and the prospects of it costing a lot to fix can be high. Caveat emptor, so goes the famous Latin phrase; buyer beware.

[1]Having the last word: Will making and contestation in Australia, Op. cit. p.2

What is an Executor and who should I appoint?

The Executor and Trustee of your Will is very important. They are a person, or persons, or professional trustee company such as the Public Trustee, who you appoint to carry out your instructions precisely as contained in your Will. They must apply for a Grant of Probate of your Will which means they must prove they are who they say they are, how much the estate is worth and that the Will is valid, and then the Court issues them with their formal seal of approval. At that point, the Executor stands in your shoes, legally speaking and can deal with your assets as if they owned them themselves. Of course, they must use those powers only to give effect to your wishes in your Will but they must also use those powers to pay debts, call in assets, commence claims that need to be commenced, and a thousand other tasks.

It is a big job, even for a simple estate. For large or complex estates it can literally be a full time job that can last for years. Many Executors do it for the love of the deceased, but they can also charge a commission for their work.

The work of the Executor includes liaising with family and business associates, coordination of beneficiary gifts and distributions, opening and closing bank accounts, advertising for creditors, organising insurance, performing an inventory (that alone can take weeks in some cases), protection of assets, preparation of statements, preparation of accounting and instructing accountants to do tax returns, selling shares and real estate, calling in debts, commencing legal action against any outstanding debts, court applications for a grant of probate, and establishment of trusts as contained in the Will.

Having an executor who you trust can also allow you to deal with your digital assets such as your email accounts, passwords and logins to your bank details, online share accounts, social media, frequent flyer programs and the list goes on. Often these accounts hold precious assets or personal information so it’s so important to give proper consideration here.

The role can last decades, particularly if young children are involved. Executors can also be personally liable for incorrect distributions or mishandling of the estate, so as you can see the role is a complex one – and so important you match the right person to the role.

Similar considerations are also appropriate when choosing a Trustee, particularly when there is a trust involving young children or minors. In this scenario you’ll also need to think about who to appoint as Guardian which can be one of the hardest decisions we can help with. Often we find this decision changes over the course of a few years as children get older, their needs change, family relationships and friendships change, another key reason for updating your estate plan every few years.

For example, whilst your best friend may be the perfect guardian today, if he or she marries a person you disapprove of then they might not be the perfect guardian tomorrow. Similarly, your sister may be the perfect Trustee of your young children’s trust today, but if she falls on hard times financially tomorrow or has a significant change to her life such as moving far away from where your children call home, it may no longer be ideal.

When it comes to an Executor, Trustee or Guardian, of course choosing the right person is paramount. Considerations include the skillset, financial and legal acumen of a person, their age, whether you choose one person or two, or more, their relationships with your beneficiaries, any conflicts of interest, and also where they live – as someone living here in WA is ideal when it comes to assisting with administration.

It may be unwise to appoint someone significantly older than you, and sometimes you need to appoint two or more to work jointly – this can help reduce the labour of each person but also allows for a check and a balance on their actions so that neither does anything which is a conflict of interest. This means that sometimes it’s not the best idea to appoint a beneficiary as executor, especially if you suspect that there are going to be fights and which then may put the executor/beneficiary in a difficult position.

You cannot force someone to accept the role as executor, it is voluntary. But once a person starts down the road of dealing with assets, and so starts acting as executor, even if probate is not yet granted, they then are locked in. It is very hard to get out of being an executor once you have started dealing with the assets and you need the approval of the Court- and you can’t just appoint anyone you want in your place.

Once we meet and work through your plan, we can discuss with you who in your circle may be the best fit for the role.

Book your free 15 min consultation

Discussing your situation over the phone is often the best way to start, and we’re pleased to offer all new and existing clients a free 15 minute phone consultation for every new matter. It’s a great opportunity to let us know more about the assistance you’re looking for, clarify your situation and walk you through how best we can help and what’s involved.

Fill in your details below

Associations