We’re in the very fortunate position to be able to work with some of Perth’s best accountants, financial planners and other legal peers, so we see the best practices used by clients each time the financial year comes to a close and a new one begins. Investing the time into sorting out important business and administrative tasks means you’re better protected and better prepared to start the new financial year.

Here are our top tips on what to consider and action as we head into the 2019 financial year, which is by no means an exhaustive list, but the top points we would highlight on both the personal and business front for this busy time of the year.

What to consider on the home front?

- Super news – make you stay across changes to legislation that hit from 1 July, including the new government incentive for over 65s to downsize their homes and make super contributions up to $300K outside the usual non-concessional (after-tax) contributions cap.

- Pension changes – from 1 July there are a number of new criteria to meet to qualify for the Age Pension or Disability Support Pension – particularly around residency periods in Australia.

- Young children? – parents will get access to a New Child Care Package from July 2, 2018, where a new Child Care Subsidy (CCS), will replace the current Child Care Benefit and Child Care Rebate, designed to be simpler and to offer more help to low and middle income families.

- Disability – with the ABS quoting around 18% of our population having some form of disability, it’s no surprise changes continue to be rolled out to better accommodate need. From 1 July, there are a number of key changes to the Disability Employment Services program designed to give Australians more say in the services they get and how they access them. If you’re after more information on the NDIS front, visit the geographic roll out in WA page to find out where and when this will be available in your area.

- Have a family trust? If so, how recently did you look at your Trust Deed and assess if it needs updating? Does the trust deed align with your personal estate planning? If the trust earns income (which is common), is the does the trust deed adequately deal with income? It is likely that trust deeds drafted prior to 2010 will need revisiting in light of Bamford’s case, which dealt with the definition of income and the trustees ability to determine what is treated as income pursuant to its powers in the trust deed, which obviously has taxation consequences. Are you up to date on your ATO Trust obligations? Don’t forget that a Trustee is responsible for registering a Trust for tax and lodging a yearly tax return regardless of the amount of net income involved, unless the ATO has advised that a return is not required.

- Have an SMSF in place? Anyone who runs a Self-Managed Super Fund (SMSF) is required to ensure that a registered SMSF auditor audits the fund annually to examine the validity and accuracy of the funds financial records and to ensure the fund is compliant with the superannuation rules. Make sure your audit obligations and financial records are in order before the end of the financial year.

- Review of your finances – whilst the terms of most mortgages are 25-30 years, the average length of a mortgage is only around four years before Australians chop and change. Do review your big-ticket items like your mortgage on an annual basis to ensure its still as competitive as it was when you signed on. Given the cash rate is at record low and has been for a record 20 months, now might be the right time to speak with a mortgage broker to see just what else might be out there.

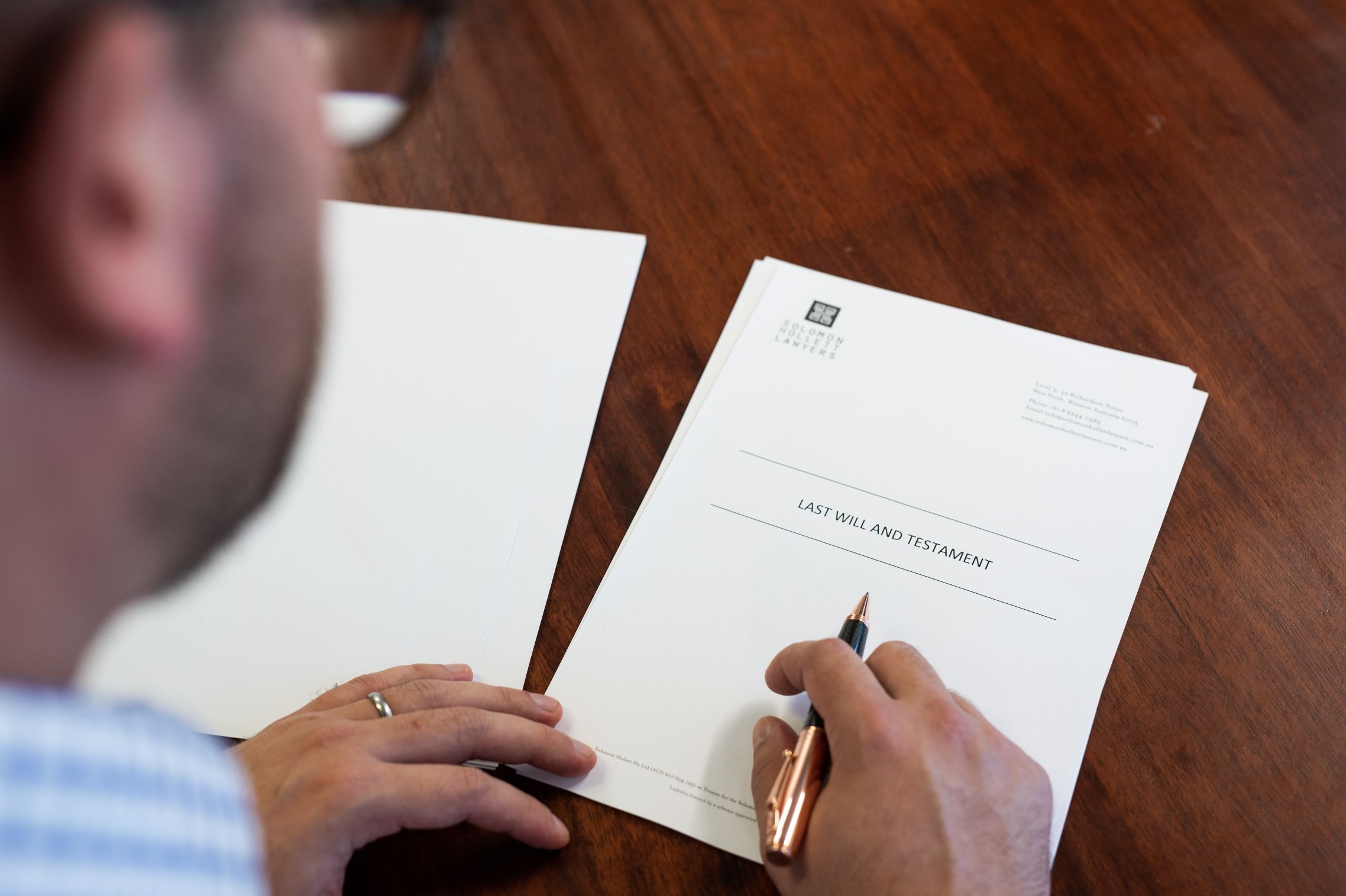

- Put yourself first – make sure your personal affairs are in order. Use the EOFY as a milestone every year to make sure your estate plan is still current, and if not then get it updated. Some things to think about might be; have you had children since your last Will was drafted or are there new relationships to consider (remembering a marriage or divorce immediately nullifies an existing Will), have you moved states, has your financial position changed in some way meaning a Trust could be a smart protection and tax effective strategy to consider? Do you have an Enduring Power of Attorney in place? Have relationships around you changed? Whatever the case may be, you should may employ smart strategies specific to your circumstances to ensure what you’ve worked so hard to achieve ends up going to the right people.

Small business owner?

- The fine print of tax time – as obvious it as it, the basics this time of year includes preparing your return, completing your quarterly or annual BAS, company obligations such as annual reports and solvency declarations, payroll tax, fringe benefits and a review of staff salaries.

- Keeping on top of the latest tax changes – speaking with your accountant is the best place to start, and you can also subscribe to the latest ATO changes via their Small Business Newsroom. Make sure that you are also up to date with small business exemptions, deductions and grants available to help small business innovate – government websites being the best place to start your research on just what is out there, as well as talking with your accountant.

- Review your insurances – make sure your insurances are current and conduct a review of your policies. Some types of policies which may be relevant to your small business include bricks and mortar policies, policies that cover the company, income and commercial risk, and others such as workers’ comp, third-party personal injury and public liability. You need to ask yourself, are my risks still what they were this time last year? If not, then ensure you’ve considered the appropriate insurances, and even seek the assistance of an insurance broker if needed. For example, with cyber-attacks on business on the increase, and with a businesses’ confidential information or client lists possible being its most valuable commodity, should you be considering cyber insurance?

- Speaking of tech – take the time to make sure you’ve backed up and your files are protected with the right levels of security in place when it comes to the storage of data.

- Review your business structure – nothing ever stays the same and as your business grows and evolves you may need to change your business structure. Talking to your accountant about this is important as a first step, then working with us on the right documentation to protect yourself and your business is key.

- Ensure your finances are in order – your balance sheet, income statement and cashflow statement will give you a pretty good picture of how you tracked this financial year against the goals you set for yourself. With any business debt, take the time to make sure you have the right business finance in place – if in doubt check with a finance broker on what is on offer and how best to make it work for you.

- What’s keeping you awake at night that you know you need to solve? – think honestly about the risks or issues you know you should address but haven’t and come up with a proactive plan to get on top of them before they get on top of you. Have you got some large debts still outstanding to you that need chasing down formally? Are your employment contracts all in place and up to date? Are your supplier contracts all in order or do a number of handshake agreements need formalising so things don’t sour? Do you have a solid succession plan in place such as a buy/sell agreement that can help ensure a smooth transition of the business when you’re ready for it down the track? Is your intellectual property well protected? Are your business processes as tight as they need to be to protect against theft or fraud?

Takes notes. There is no point reinventing the wheel every year. Generally speaking, the actions you take for your business and your personal life at the EOFY will be the same or similar from year to year, but you will be hard pressed to remember what exactly you did a year down the track. Remember to always seek the advice of professionals on all of the above, and note down the processes you have in place, to make each EOFY year easier than the last!

Related Articles

Your guide to setting up a Trust

Who pays to challenge a Will?

The benefits of establishing a Trust

Brandon Hetherington has considerable experience across the realms of Wills and estate planning, probate and family provision claims, property law, commercial law and litigation. Brandon’s work has seen him appear frequently across the Magistrates Court, District Court, Supreme Court, and the State Administrative Tribunal.