Our areas

of expertise

Solomon Hollett Lawyers are the leaders in inheritance law in Western Australia. We offer advice and expertise that includes Wills and estates planning, estate litigation and inheritance disputes, estate administration, power of attorney and business succession. We are also experts when it comes to commercial law , specialising in commercial disputes, partnership disputes, commercial leasing, property, contract drafting and partnership agreements.

Contact usInheritance

disputes

Inheritance disputes are rising as family dynamics and asset structures grow more complex. We protect clients facing challenges to their entitlements and help those seeking to right a wrong. From negotiation and mediation to court representation, we provide strategic guidance and unwavering support to achieve the best possible outcome.

Contesting a Will

Challenging a Will can be an emotional and complex process. If you’ve been unfairly left out or received less than expected, we can help you understand your rights and options. Our team will assess your claim, guide you through Probate Court, and work to secure a fair outcome. We strive to protect what’s rightfully yours while ensuring the final wishes of your loved one are honoured.

Defending a Will

If you’re an Executor or beneficiary facing a challenge to a Will, defending it can be overwhelming. We provide strong legal support to uphold the deceased’s wishes and ensure the estate is distributed correctly. Whether through mediation or court proceedings, we work to protect your rights, preserve the integrity of the estate, and minimise family disputes.

Inheritance disputes & estate litigation

Estate disputes can be legally complex and emotionally draining. Whether you’re contesting a Will, defending one, or facing conflicts over estate administration, we offer strategic legal guidance and strong representation. Our focus is on resolving disputes efficiently and fairly while safeguarding your rights and the estate’s integrity.

Wills and

estates planning

We specialise in Wills, estates, succession, and inheritance law, helping clients create, preserve, and transfer wealth to protect their loved ones. Our expertise covers Wills, Powers of Attorney, Testamentary and Discretionary Trusts, and business succession planning, ensuring tailored strategies that secure the right legacy for generations to come.

Estate planning

Secure your future with comprehensive estate planning. You can ensure your assets are managed and distributed according to your wishes, both during and after your lifetime, protecting your legacy and providing for your loved ones.

Power of Attorney

Safeguard your financial and property interests during your lifetime. Appoint a trusted person to make important decisions on your behalf when you are unable to, ensuring your affairs will be handled with care and efficiency.

Superannuation

Maximise your retirement savings. We provide legal guidance on incorporating superannuation into your estate plan, ensuring your retirement benefits are passed on effectively and efficiently.

Testamentary Trusts

Establishing a Testamentary Trust in your Will can safeguard the transfer of your estate assets, providing long-term security and support for your beneficiaries in a protective structure.

Estate administration

Managing a deceased estate can be complex and time-consuming, but our experienced team at Solomon Hollett Lawyers is here to guide you through the process with care and clarity. We assist executors and beneficiaries in handling estate administration, ensuring compliance with legal requirements, and resolving any disputes that may arise.

Commercial disputes

We specialise in commercial dispute resolution and litigation, helping businesses navigate conflicts at any stage—from early negotiation and settlement to trial and appeal. With experience across complex business structures and industries, we provide strategic, pragmatic legal solutions to resolve disputes efficiently and protect our clients’ commercial interests.

Bankruptcy & insolvency

Navigating bankruptcy or insolvent debtors can be overwhelming. Our team offers clear guidance and robust support, from negotiating with creditors to managing liquidations and bankruptcy notices.

Mediation & arbitration

Mediation and arbitration can ease the stress of commercial disputes. Our team helps you find practical, out of court solutions that protect business relationships and achieve fair outcomes.

Commercial litigation

When disputes escalate, our commercial litigation team provides determined representation and strategic advice with a view to resolving conflicts in your favour, handling a wide range of litigation matters.

Partnerships disputes

It is almost inevitable that a dispute will arise in partnerships at some stage. Our lawyers ensure your partnership agreements cover all potential disputes, including mechanisms to resolve those disputes, tailored to your partnership’s unique needs.

Contract disputes

Understanding your contractual rights and obligations is crucial. We offer insightful legal counsel to safeguard your interests in contract negotiations.

Business fraud recovery

Business fraud can have severe consequences. We act swiftly to recover assets, employing civil remedies and guiding you through interactions with enforcement authorities to protect your business.

Commercial law

We provide strategic, pragmatic legal solutions for businesses of all sizes across diverse industries. From contracts and business structures to acquisitions, succession, and disputes, we handle transactions, leases, loan agreements, franchising, and more. Whether drafting, negotiating, or advising, we help clients navigate complex legal matters with clarity and confidence.

Commercial leasing

Secure and strategic leasing solutions. Get advice on commercial leasing, ensuring your agreements are clear, favourable , and legally sound.

Commercial property

Navigate property matters with confidence. We offer comprehensive legal support for commercial property transactions, including acquisitions, sales, leasing and development.

Business sale

Experience smooth business transitions. Our business lawyers will guide you through the complexities of buying or selling a business, ensuring a seamless and successful transaction.

Contract drafting & review

Draft robust and clear contracts. Our lawyers can help you in professional contract drafting to prepare plain english contracts designed to protect your interests and ensure clarity in all business dealings.

Partnership agreements

Build strong and fair partnerships. Work with us to develop tailored partnership agreements that outline the roles, responsibilities, and expectations of each party, fostering successful collaborations.

Our resources

Top estate planning mistakes we see far too often

Estates can frequently become battlegrounds for contention and disagreement when you don’t effectively plan and strategise your Wills and estate plans. We have identified the top 12 pitfalls we commonly observe when it comes to Wills and estate planning so that you can protect yourself, your loved ones, and your all important legacy.

The Little Black Book on all things succession law

We recently put together a Little Black Book on the inside running on succession law, Wills and estates and inheritance disputes here in WA. Initially written to help lift understanding of this space across our accountant and financial planning peers, we’ve been inundated with requests from our clients. We’re thrilled to share this copy with you, enjoy the read.

The 2025 Wills & estate planning guide for WA

There have been a number of transformations in the WA Wills and estates arena recently. This updated guide highlights key developments and trends, providing valuable context on how they may influence your situation. Read crucial insights into Wills and estate planning, as well as litigation in Western Australia.

Top business mistakes not to make

All too frequently, clients approach us with commercial disputes that stem from minor business blunders that could easily have been avoided. So, we’ve made a list of the top 10 business mistakes we see and included helpful tips and methods to keep you from facing the same issues.

Commercial disputes and litigation guide

If you’re a business owner or decision-maker in Western Australia, this is for you. Our updated guide addresses your questions about the most effective methods for safeguarding against commercial disputes and managing them if they arise. It also covers various strategies for resolving conflicts and, in cases where litigation becomes the only way forward, outlines the process.

Navigating Western Australian inheritance law – your FAQ guide

The ultimate guide answering the key legal questions from over 30,000 Western Australians when it comes to all things inheritance, Wills, estates and succession. How best to protect assets and secure legacies is covered here as we navigate you through the most common questions, the greatest myths and the biggest mistakes we see time and time again.

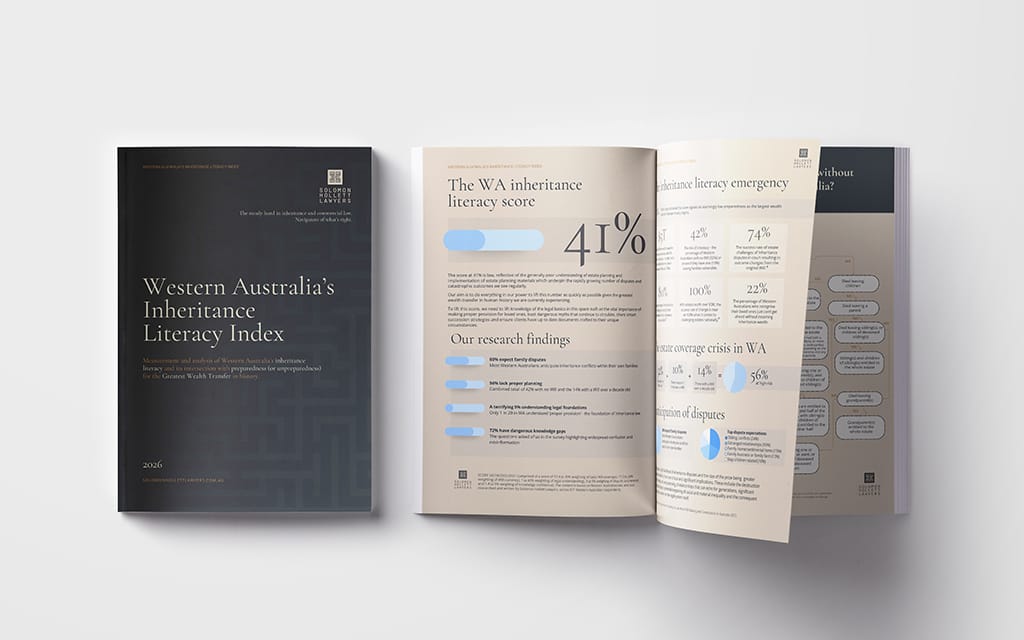

Western Australia’s Inheritance Literacy Index

Welcome to our Inheritance Index – our measurement and analysis of WA’s inheritance literacy and its intersection with preparedness (or unpreparedness) for the greatest wealth transfer in history. The score is out of 100 – based on Will and estate plan coverage, legal understanding, dispute awareness and knowledge confidence of 971 West Aussies we surveyed. Our job is to lift this year on year, and this short Index has a few pointers on how.

Get the right legal support for your needs

Whether you’re planning for the future, resolving a dispute, or protecting your business and assets, we’re here to help. Our experienced team provides strategic, practical legal solutions tailored to your situation. Contact us today to discuss how we can assist you.

Contact us

Postal Address

PO BOX 840, West Perth,

Western Australia 6872

Phone

08 6244 0985

Your legal journey begins here

Whether you have questions about inheritance disputes, Wills, or estate planning, our team is here to help. Reach out today to discuss your legal needs and discover how we can support you with clear, practical advice.